Crocs (CROX): Undervalued, Misunderstood, and Ready for a Breakout

The Investment Case for a Brand Everyone Recognizes but Wall Street Undervalues

If you've ever dismissed Crocs (NASDAQ: CROX) as "that ugly shoe company" or written it off as a passing fad, you're not alone. I initially did too. But diving into the numbers reveals something that doesn't match this perception: a cash-generating machine trading at a serious discount to both peers and intrinsic value.

Let me walk you through why Crocs deserves a closer look, and why its combination of strong financials, smart capital allocation, and consistent outperformance makes it one of the most compelling value opportunities in today's market.

If you're interested in exploring stock opportunities like Crocs, Inc., you can check out my stock screening app here.

The Numbers Don't Lie: Strong and Getting Stronger

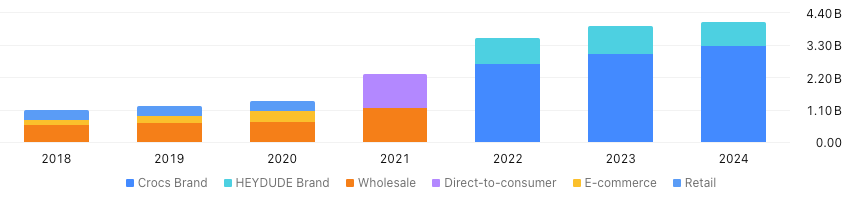

For 2024, Crocs delivered another record year: $4.1 billion in revenue (up 4% year-over-year) with adjusted gross margins expanding to 58.8% (up nearly 3 percentage points from 2023). The core Crocs brand grew an impressive 8.8%, offsetting softer performance from the HEYDUDE acquisition.

What jumps out immediately is their operational efficiency. Operating margins consistently hover around 20% – exceptional for a footwear company – while generating free cash flow of $923 million in 2024 alone. That's over 22% of revenue converted directly to free cash flow, a level most retailers can only dream about.

Capital Allocation: Playing Both Offense and Defense

Many companies talk about "returning value to shareholders," but few execute as effectively as Crocs has over the past three years:

In 2021, they issued long-term debt at historically low rates (below 4.5%) specifically to fund a $1 billion share buyback – perfect timing before interest rates spiked.

As shown in the figure above, Crocs timed its capital moves brilliantly - taking advantage of historically low interest rates to issue bonds at 4.13% and 4.25% (maturing in 2029 and 2031) to fund shareholder returns when their share price was significantly undervalued.

In 2022, they used $1.6 billion in debt to acquire HEYDUDE, a complementary casual footwear brand, diversifying their product mix (though with mixed results so far).

Since then, they've been systematically paying down debt ($323 million repaid in 2024) while continuing aggressive share repurchases ($551 million spent buying back 4.3 million shares in 2024).

The real kicker is what's still on the table. In February 2025, the board authorized another $1 billion for buybacks, bringing the total authorization to $1.3 billion – more than 25% of the company's current market cap. That's a serious vote of confidence from management and provides significant support for the stock.

The steady reduction in share count has been a consistent feature of Crocs' strategy since 2018, with only a minor share issuance in 2022 that was quickly offset by renewed buybacks. With free cash flow reaching $923 million in 2024 alone, the company's $1.3 billion buyback authorization could theoretically be completed in under 18 months without impacting its debt reduction goals.

With the company's cash generation strength, they can maintain this buyback pace while still steadily reducing debt – a rare combination in today's market.

A Valuation Disconnect That's Hard to Ignore

If Crocs were trading at typical industry multiples, we wouldn't be having this conversation. But the disconnect between its operational excellence and current valuation is stark.

Let's put this in perspective. Crocs currently trades at a P/E of approximately 5.55 – the lowest among key footwear competitors. The next closest is Skechers at 11.25 (nearly double), while brands like On trade around 50x earnings.

Its price-to-sales ratio of roughly 1.25 is similarly depressed compared to peers, as is its EV/EBITDA ratio. This valuation gap exists despite Crocs demonstrating:

Higher gross margins (57.9%) than many competitors

Operating margins (~20%) that lead the industry

Superior inventory turnover, indicating efficient operations

Best-in-class ROE and ROIC metrics, well above the 10% "good business" threshold

The market is essentially pricing Crocs as if its current performance is a temporary blip before an inevitable decline. The data simply doesn't support this pessimism.

Additional high-value points to include:

Analyst consensus: Despite the market's skepticism, the professional analyst community has a significantly more positive outlook, with an average price target of $124 (ranging from $99 to $153) - suggesting upside potential of 30-60% from current levels.

Growth trajectory: Unlike a fading trend, Crocs has demonstrated consistent revenue growth over multiple years, with record annual revenues of $4.1 billion in 2024, representing a 4% increase year-over-year.

Cash flow strength: Crocs generated $923 million in free cash flow in 2024 (approximately 22% of revenue), demonstrating exceptional cash conversion.

Historical volatility misconception: While the stock has experienced significant price movements around earnings releases, the underlying business fundamentals have remained consistently strong, suggesting that market perception - rather than business reality - is driving the valuation gap.

International expansion potential: With China recently becoming Crocs' second-largest market (representing about 6% of revenue), the company has demonstrated its ability to successfully expand globally, providing additional growth avenues that aren't fully reflected in the current valuation.

If you're interested in exploring stock opportunities like Crocs, Inc., you can check out my stock screening app here.

DCF Analysis: Substantial Upside Even With Conservative Assumptions

When I run a discounted cash flow analysis on Crocs, the results reinforce how undervalued the company appears. Using a conservative 15% discount rate to reflect required returns above the S&P 500 average:

Here are the key assumptions used:

Initial cash: $180 million and debt: $2.315 billion (consistent across all scenarios)

Initial free cash flow: $850 million (bear), $920 million (base), and $1 billion (bull)

Five-year growth rates: 3% (bear), 5% (base), and 10% (bull)

Terminal growth rates: 2% (bear) and 3% (base/bull)

Even in a bear case scenario (assuming just 3% five-year growth and 2% terminal growth), the analysis suggests a 13% IRR – still solid. In the base case (5% five-year growth, 3% terminal growth), the IRR hits 15%, while a bullish scenario points to 18% returns and potential share prices up to $126.

What's particularly encouraging is that this analysis doesn't fully factor in the accretive effect of ongoing share repurchases, which should further boost per-share value. With Crocs' aggressive buyback program ($551 million spent in 2024 alone and a fresh $1.3 billion authorization), the company is steadily reducing share count, which mathematically increases the per-share value beyond what my base DCF model projects. These buybacks effectively allocate capital to the most undervalued asset (their own shares), creating a compounding effect on shareholder returns that isn't fully captured in the static IRR calculations.

The company's financials are straightforward with no accounting tricks or one-off gains driving results (apart from a recent tax write-back that temporarily inflated net margins). This clean financial profile gives greater confidence in the DCF inputs and projections.

Bear case risks like potential tariff impacts (estimated at $11 million gross profit reduction in 2025) are considered transitory rather than permanent structural issues, which supports the long-term valuation thesis even with conservative growth assumptions.

Beyond U.S. Borders: The International Opportunity

One persistent misconception about Crocs is that it's primarily an American mall brand. While North America does account for over 50% of revenue, the international growth story is compelling and often overlooked.

China has emerged as Crocs' second-largest market, now contributing approximately 6% of total sales. This international diversification not only provides growth opportunities but also some insulation from regional economic fluctuations.

The brand mix tells an interesting story too. While the HEYDUDE acquisition created a second revenue stream, that brand has remained relatively flat at around $900 million annually. Meanwhile, the core Crocs brand continues to grow steadily and generates more than 75% of total revenue.

This concentration presents both a risk (limited diversification) and an opportunity (focus on their strongest brand). The lackluster performance of HEYDUDE suggests management should prioritize revitalizing this acquisition or consider doubling down on the core Crocs growth story.

Manufacturing: The Offshore Risk Factor

Crocs outsources 100% of its manufacturing to third-party partners, primarily in Vietnam (53% of production) and China (around 15% of U.S. imports), with newer capacity in India (now at 10% of production) and other countries. This creates tremendous operational flexibility and keeps fixed costs low compared to vertically integrated competitors, but it also introduces geopolitical and supply chain vulnerabilities.

For 2025, new tariffs on imports from China and Mexico are expected to reduce gross profit by approximately $11 million – about 25 basis points of margin impact. Management is addressing this through ongoing supplier diversification, but it remains a key risk to monitor.

The footwear industry as a whole faces similar challenges – over 99% of all shoes sold in the U.S. are imported – but Crocs seems relatively well-positioned with its Vietnam-centered production and ongoing diversification efforts.

Analyst Sentiment: The Professionals Agree

Wall Street seems to be waking up to the Crocs story. Current 12-month price targets from 12 analysts range from $99 to $153, with an average of $124 – well above recent trading levels.

Forecasts for 2025 suggest modest revenue growth around 5% to $4.18 billion, with projections for 2026-2028 indicating continued 2-3% annual growth – roughly in line with inflation. These conservative growth expectations are baked into the current valuation, creating potential upside if Crocs can sustain its recent momentum.

Why the Discount Persists: Understanding Market Skepticism

If Crocs is such a strong performer, why does it trade at such a discount? Several persistent concerns hang over the stock:

Brand image concerns: The polarizing "love it or hate it" aesthetic of Crocs makes investors nervous about long-term staying power, despite evidence of sustained demand.

Perceived trend reliance: There's persistent fear that the "clog trend" could fade, though Crocs has successfully navigated fashion cycles for over two decades now.

HEYDUDE underperformance: The lack of growth from this acquisition raises questions about management's ability to diversify beyond the core product.

Supply chain exposure: Heavy reliance on Asian manufacturing introduces both tariff and geopolitical risks.

Historical volatility: Crocs has experienced boom-bust cycles in the past, leading to lingering skepticism about sustainability.

While these concerns have some merit, they seem more than adequately priced into the current valuation. The margin of safety at current levels provides substantial protection against these risks.

The Bottom Line: A Classic Value Opportunity

Crocs represents a classic case of market perception lagging business reality. The numbers tell the story of a highly profitable, cash-flowing machine with smart capital allocation and clear competitive advantages – yet it trades at deep discounts to both peers and intrinsic value.

Whether you're a value investor looking for quality at a reasonable price, or an income-via-buybacks seeker, Crocs offers a compelling opportunity at current levels. The combination of continued execution, aggressive share repurchases, and potential multiple expansion could drive significant returns in the coming years.

Sometimes the most profitable investments are the ones hiding in plain sight – or in this case, on millions of feet worldwide.

Resources:

Disclosure: This article represents analysis only, not investment advice. Do your own research before making any investment decisions.